Constitutional

We hold, therefore, that § 6601(f) (3) applies and that plaintiff, having paid its accumulated earnings tax within 10 days of demand, should not have been charged interest.9

Section 6601(a): Even if § 6601(a) applies,10 as the Government contends, taxpayer is nevertheless entitled to recover. Under that section, interest accrues from the “last date prescribed for payment.” § 6601(c) states that

For purposes of this section the last date prescribed for payment of the tax shall be determined under chapter 62 [with the application of certain rules].

Chapter 62 “Time and Place for Paying Tax” §§ 6151-6166, details the time and place for payment. Since, as we have pointed out, the accumulated earnings tax is not reportable on any return, but rather “result[s] from the initiative of the tax collector and not, as is more usual with other income taxes, from the initiative of the taxpayer” (Govt.Br. at 5), it follows that this tax becomes payable only upon notice and demand by the Internal Revenue Service. For that reason, the part of chapter 62 we deem applicable is § 6155, which states that:

Upon receipt of notice and demand from the Secretary or his delegate, there shall be paid at the place and time stated in such notice the amount of any tax (including any interest, additional amounts, additions to tax, and assessable penalties) stated in such notice and demand.

Because § 6155 prescribes the last date for payment of the accumulated earnings tax, none of the subdivisions of subsection 6601(c), giving rules for determining the date prescribed for payment, is applicable.11 Under § 6601(a),

Page 709

accordingly, taxpayer is liable for interest on the unpaid § 531 levy only between the receipt of notice-and-demand and payment.

Credited for debit, and to debits credit in settlement of payment. receipt of notice-and-demand and payment.

Taxpayer has made timely payment under either § 6601(a) or § 6601(f) (3), and it is entitled to recover that amount of its payment which represents the interest charged upon the assessed accumulated earnings tax.12 Judgment is entered for plaintiff to that effect. The amount of recovery will be determined under Rule 131(c).

CONCLUSION OF LAW

Upon the foregoing opinion, which contains the necessary findings of fact made part of the judgment herein, the court concludes as a matter of law that plaintiff is entitled to recover, and judgment is entered to that effect, with the amount of recovery to be determined pursuant to Rule 131(c).

Necessary andor of lien.

Directives Annual.

Secretaries Annual.

Certainties Annual.

Government

Beneficiary Lender:

United Kingdom

United States

Russia

China

Japan

Italy

Norway

France

Professional services re examinations of June 30, 2020, and report:

Principal, 1 day, at $21350 …..

In charge accountant, 114 days, at $11235.40 22.50

Assistants, 5 days, at $125 .. 8137.50

Office, 4 days, at $ 110 …… 5340.00

.. Total ………………………………2,320.40

…998033+ S . Doc. 181 , 67-2- -37

$ 310 fee

13,020

Syria

Isreal

Iran

Germany

Poland

Austria

Antarctica

Trustee Serve:

Trust Accounts equal to escrow accounting of Tax & Interests.

Trustor: The Federal Government of Earth

Lender:

Auction Court House andor steps total GDP.

Expects Grantors demand

Trust Accounts equal of Escrow for expected Taxes and Insurance annual. [Deed | Mortgage | Other]

Particulars:

15 trillion in expenditures:

5 trillion in excess of:

Clients deposit

received as security for container.

Eliminates the is a debit to liabilities.

Practice:

10 trillion in expenditures:

5 trillion in excess of:

Person [Individual] andor Officer Volunteer.

10 trillion in expenditures:

5 trillion in excess of:

Customers deposit

received as security for container.

Eliminates the is a debit to liabilities.

Person [Individual] andor Officer Volunteer.

10 trillion in expenditures:

5 trillion in excess of:

Privaate

Expenditures annual.

25 trillion in expenditures:

5 trillion in excess of:

The Country bank of needham

Trade Policy –Customs tariff designed for maximum revenue; three columns conventional, statutory (general) and maximum GATT signatory, Products may be subject to prior import license.

Billions of Dollars

2021-22: Exports, 3.988.9; U.S. Share, 95.0 (46.6%)

2021-22: Imports, 1.870,9; U.S. Share, 392.9 (54.9%)

2022-23: Exports, 5.988.9; U.S. Share, 95.0 (46.6%)

2022-23: Imports, 870,9; U.S. Share, 392.9 (54.9%)

Principal imports from U.S.: Technologies in Government, business, trade, wealth, industrial machinery, ancient works, coffee, gold, silver, grain, barley, television, purchase power, power authorities,

Major export has Guaranties for the US dollar, from the interest growth ed out of original assets

counter party credit risk

Levy on

Capital one,

General Electric Credit union

Loss is account by loss Provision from inner policy procedures.

bank profitability

return on equity

level of capital

Payroll department to Profile.

Directives Annual.

Expenditures annual.

Secretaries Annual.

Expenditures annual.

Certainties Annual.

Expenditures annual.

Eliminates

the is a:

debit to liabilities.

Paid to account.

Trustee

Certainties Annual.

Avoiding: Restraint of the people Loss too Risk, from entire or partial loss.

Expenditures annual.

48,474.30

expects $ 22,110,20 in gains this from less then 75% waste. the 25% in weighted tonnage poll stranger law of struggle parole demure value ratio tells pool binary. total 100% is 24,237.15 however normally gives 50% without extra growth,

Eliminates

the is a:

debit to liabilities.

24,237.15

Paid to account.

Trustee

NEW YORK, September 22, 2024.

Alien Property Custodian,

bureau of sales ( United Brush Manufactories ),

to Emery ,Varney ,Blair& Hoguet, Dr.:

To services rendered to the bureau of sales in connection with the patent and trademark situation of the above-mentioned concern, including preparation of report for the bureau of sales, preparation of demands and information reports relating to the same, and miscellaneous services incidental thereto.$550

Disbursements:

To recording deeds in the United States Patent Office .. $17.00

To additional prints in connection with trade-mark applications. 15.00

To notary fees, car fare, and postage… 9.15

Total…. 41.15

Received payment …………………………….. 591.15

Recorders fee

Value ratio for the

24,237.15

dr 600,000

cr 2,210,000

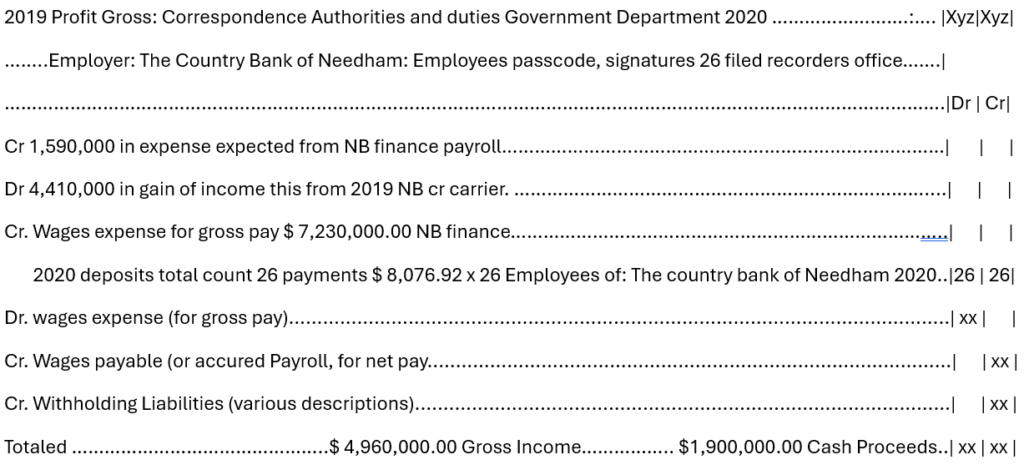

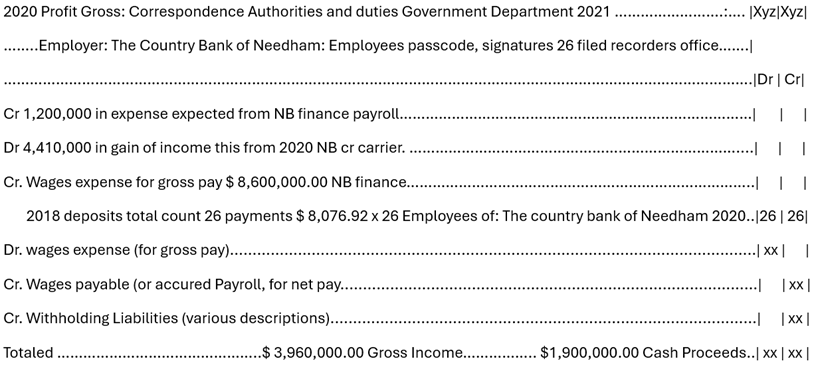

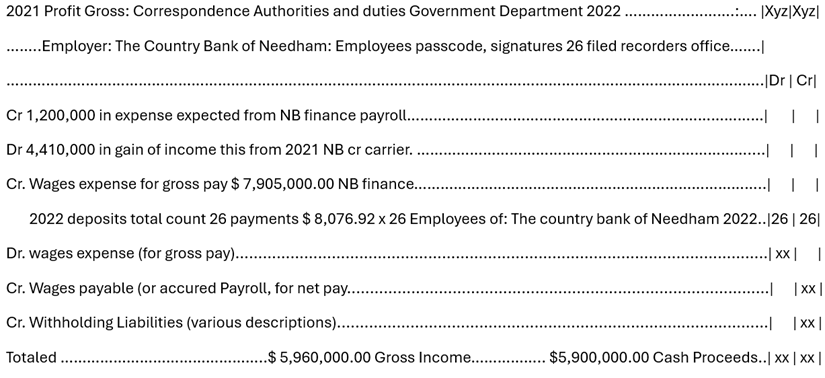

Employee

Cr 1,200,000

Dr 4,410,000

21

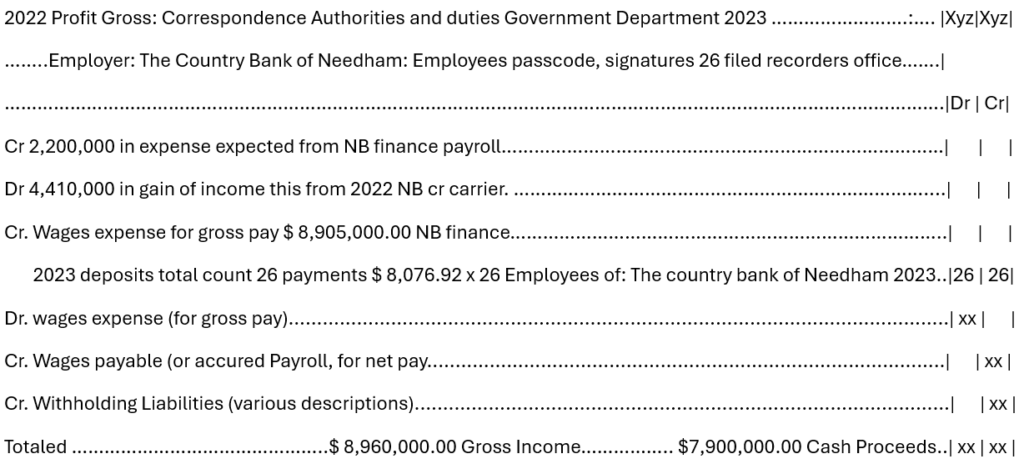

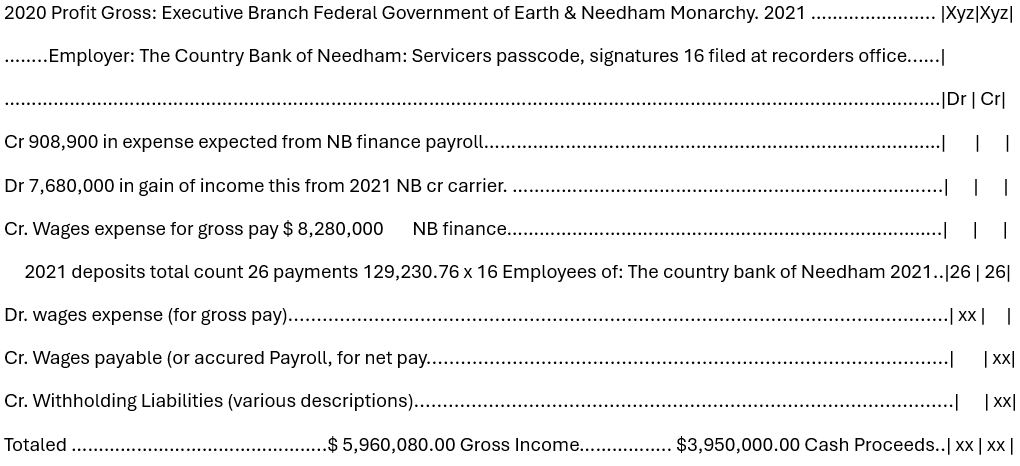

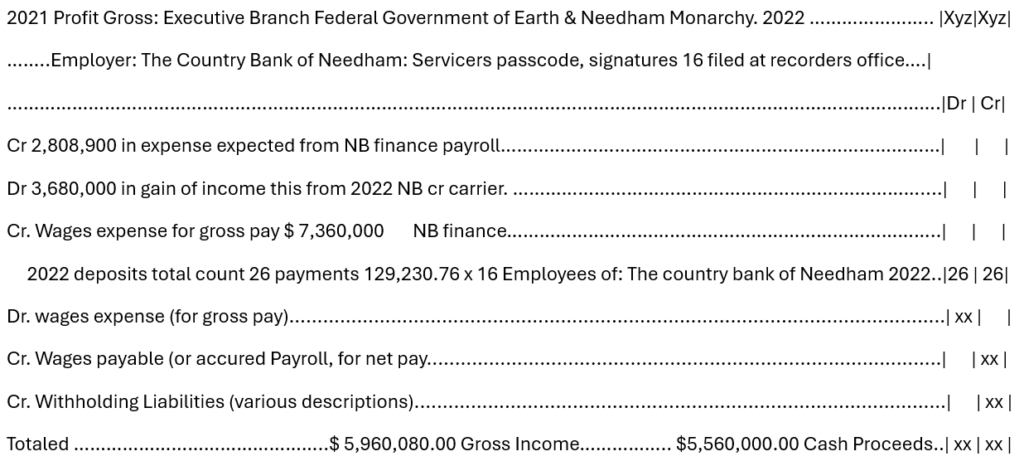

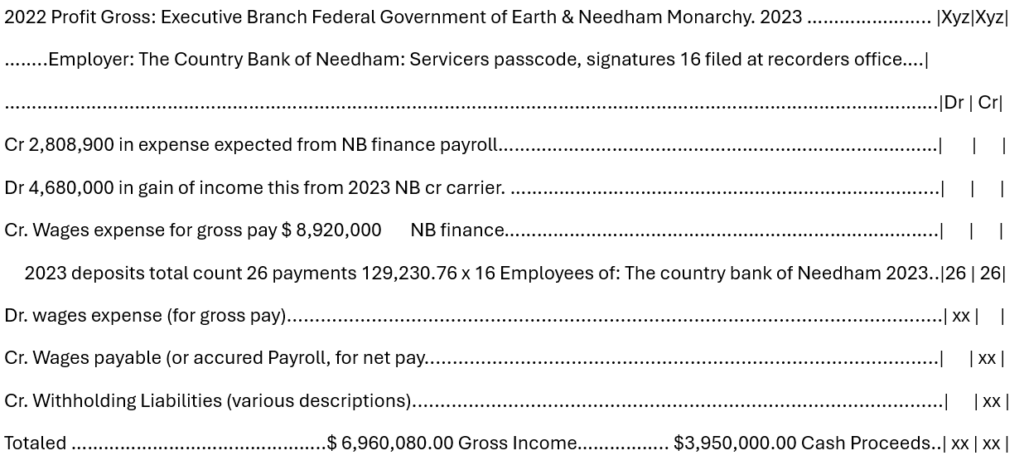

Dr. wages expense (for gross pay)………………………………………| xx | |

Cr. Wages payable (or accured Payroll, for net pay…………| | xx |

Cr. Withholding Liabilities (various descriptions)…………….| | xx |

Wages Expenses Proceeds for sales Debit.

Dr 210,000.00 ……………………………… form 49.

Compensation expenses

Cr 1,200,000

$ 310 fee

13,020

Professional services re examinations of June 30, 2020, and report:

Principal, 1 day, at $560 …..

In charge accountant, 114 days, at $376.64 22.50

Assistants, 5 days, at $200 .. 1137.50

Office, 4 days, at $ 162 …… 340.00

.. Total ………………………………2,798.64

…99803- S . Doc. 181 , 67-2- -37

x26 = 72,764.64

x26 1,891,880.64

Tax Sales proceeds 926.48

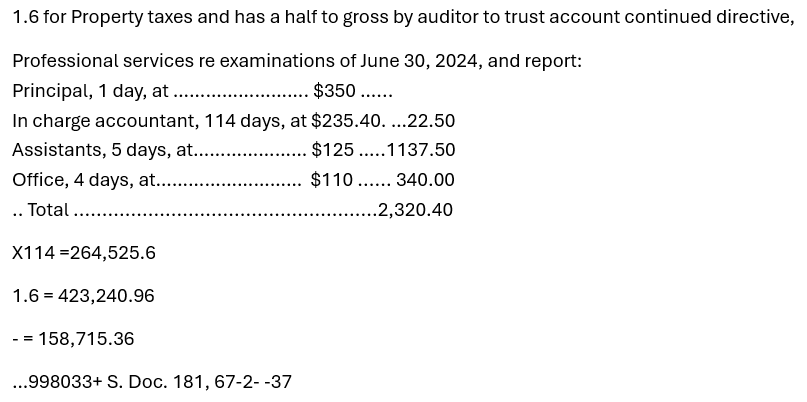

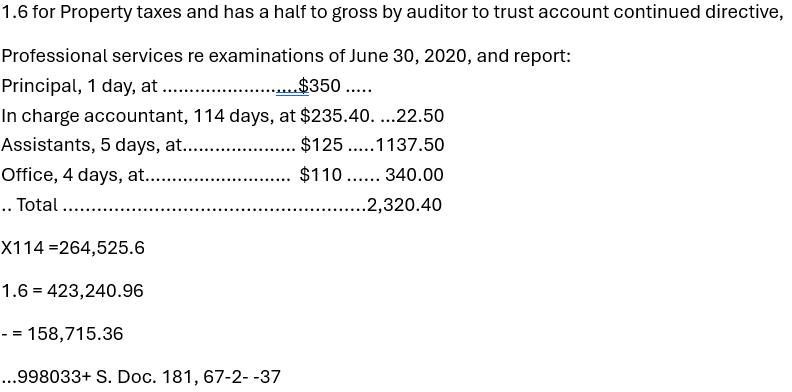

463.24 is 1.6 for Property taxes and has a half to gross by auditor to trust account continued directive,

210 | 136.24 \75 \42

Professional services re examinations of June 30, 2020, and report:

Principal, 1 day, at $350 …..

In charge accountant, 114 days, at $235.40 22.50

Assistants, 5 days, at $125 .. 1137.50

Office, 4 days, at $ 110 …… 340.00

.. Total ………………………………2,320.40

…998033+ S . Doc. 181 , 67-2- -37

x26 60,330.40

x26 1,568,590.40

$ 310 fee

13,020

52 Fridays

Internal Control Policy

Taking all Cash discounts possible.

Associate Title Agency

Net Income: 903 Trillion dollars

Revenues: 301 Trillion

Expenses: 251 billion.

Cash….880

Dr. Discounts. 120

Cr. Short term debt …. 1000

Dr Interest Expense ….XX

Cr Discount on short term debt…xx

Cash Proceeds

Maturity of

Unshipped Proceeds

Dr: Cash…………………………………………………………………………………….xx

Cash….880

Dr. Discounts. 120

Cr. Long term debt …. 1000

Dr Interest Expense ….XX

Cr Discount on Long term debt…xx

Cash Proceeds

Maturity of

Unshipped Proceeds

Dr: Cash…………………………………………………………………………………….xx

63 + 21 covers all four sides the smaller profits.

Cash………………………………………………………….880

Cr. Discounts…………………………………………. 120

Dr. Short term debt …………………………….. 1000

Cr Interest Expense …………………………………………XX

Dr Discount on short term debt…………xx

Cash Proceeds

Maturity of

Unshipped Proceeds

Cr: Cash…………………………………………………………………………………….xx

On long term debt as in 5 years,

Borrower:

Dr Cash….880

Dr. Discounts. 120

Cr. Short term debt …. 1000

Dr Interest Expense ….XX

Cr Discount on short term debt…xx

Cash Proceeds

Maturity of

Unshipped Proceeds

Dr: Cash…………………………………………………………………………………….xx

Dr: Unearned Subscriptions revenues…….Current liabilities….xx

Head office = three day charges immediate payment of Payroll.

elected September 25, 1997; resigned December 11, 2023; fee, 480 none.

Accounting:

Haskins & Sells, paid from proceeds.. …………………………….$150.00

Perley Morse & Co., paid by company. ………………………….2,986

Printing:

Acquiring: .

Frank Presbrey Co., paid from proceeds……………………………142.40

Frank Presbrey Co., paid from proceeds…………………………… 502.16

George P. Wagner, paid from proceeds……………………………..750

deed of trust………………………………………………………………………… $100.95

Maturity of

Unshipped Proceeds

Dr: Cash…………………………………………………………………………………….xx

Balance sheet………………………………………………………………………….Income Statement

Assets = Liabilities + Owners equity <-Net Income = revenues – expenses

A. Gross Method

1.record purchases

Inventory……………..Accounts……………………………………………………….. Purchases

+1000…………………..Payable………………………………………………………….. Discounts

…………………………….-1000……………………………………………………………….+20

…………………………………………………………*(A reduction of cost of goods sold)

2. Pay with discount period.

3. Pay after the discount period.

Cash ……………… Accounts

-1000 ……………..Payable

………………………… -10000

B. Net method.

- record purchases.

Inventory………. Accounts

+980 ……………… Payable

………………………… +980

2. Pay within the discount period:

Cash ……………….. Accounts

– 980 …………….. Payable

………………………..-980

3. Pay after the discount period:

Cash ……………… Accounts………..Purchase

-1000……………..Payable……………Discounts

………………………..-980…………………Lost

…………………………………………………..-20

Address : 239 Fourth Avenue, New York City.

Authorized capital: $ 100,000 common.

Enemy interest : $96,000 common.

Counsel: J. D. Brodhead, Washington, D. C.

Counsel fees:

J. D. Brodhead, paid from proceeds of sale….

Patent counsel

Board of directors ( fee per meeting, $ 20 ):

………………………………………………………………………………………………………Elected. ………………..Resigned. ………………………..Fee.

R. L. Montague, 619 Mutual Building, Richmond , Va ………. Sept. 23, 1998……..Oct. 8, 1998 …………………..$440

R. Grayson Dashiel, 621 Mutual Building, Richmond, Va … ..do . ……………………….do . ………………………………….400

Officers:

R. L. Montague, president ….. None.

R. Grayson Dashiel, secretary and treasurer (at $ 100 per month). $ 1,100.00

Auditing:

American Audit Co., paid by company………….. $ 289.00

Appraising:

E. W. Hunter, paid by company………………………….$25.00

Miscellaneous:

Paid by company. …………………………………………………$100.30

Disposition:

Property returned under section 9 claim, October 8 , 1998.

elected September 25, 1997; resigned December 11, 1998; fee, none.

Accounting:

Haskins & Sells, paid from proceeds.. …………………………….$150.00

Perley Morse & Co., paid by company. ………………………….2,986

Printing:

Acquiring: .

Frank Presbrey Co., paid from proceeds……………………………142.40

Frank Presbrey Co., paid from proceeds…………………………… 502.16

George P. Wagner, paid from proceeds……………………………..750

deed of trust………………………………………………………………………… $100.95

Maturity of

Unshipped Proceeds

Dr: Cash…………………………………………………………………………………….xx

A.Cash down payment of value or trade …………Amount $

B.1st Deed of trust at _________% interest for _____years….Amount $

Finance Company

C.2nd deed of trust at_________% interest for _____years….Amount $

loan carrier by seller

D.was other type of financing involved not covered in

type________at_______%Interest_______years………………..Amount $

f. total purchase price or acquisition price, if exchanged add A through e……Amount $

4.was any type of personal property included in the purchase, subject to local property tax? a___ b____

5. transfer is by

A. __ Deed B. __ Contract for sale

C. __ Forecloser Instrument D. __ Other-Explain. _______

6. was only partial of the interest in the property transferred ……… a __ YES b. __ NO if yes enter the amount transferred $ _____________

7. Date of transfer______(if same as recording date enter “see recording date” or B.__ if an inheritance. Date of Death__________

8. is or will the property be producing income. …….a. __ Yes b. __ No

9. If yes to income. A. __ Lease B.__ Contract. C. __ Mineral Rights. D. __ Other explain. _______

O. Did the transfer of this property involve the trade or exchange of other real property… a. __ Yes b. __ No

- is this property intended as your principal residence….. A.__Yes b.__ No

- if “yes occupancy _______________________ (if same as recording date, enter “see recording date”) or intended date of occupancy________________

Sent to escrow accounts:

Estimated warranty expense:

Escrow releases funds for:

Trust account.

revenue from the sale is recorded.

1/6

Municipal civil service commission

for the purpose of employing per diem

and experts

examiners

monitors

Public

Department of finance.

Bureau of Municipal investigation and statistics.